Previous Story

DESIGNING FOR RESILIENCY – THE NEW FACE OF SUSTAINABILITY

Posted On 30 May 2024

Comment: Off

By: Frank Came

Although the fact that our weather patterns are changing is not headline news, the rising frequency and severity of extreme weather events are of growing concern.

Over the past three decades, there have occurred unprecedented wildfires and floods across much of North America and elsewhere that have devastated whole communities and cost billions of dollars of damage, not to mention unfortunate numbers of deaths to residents and first responders.

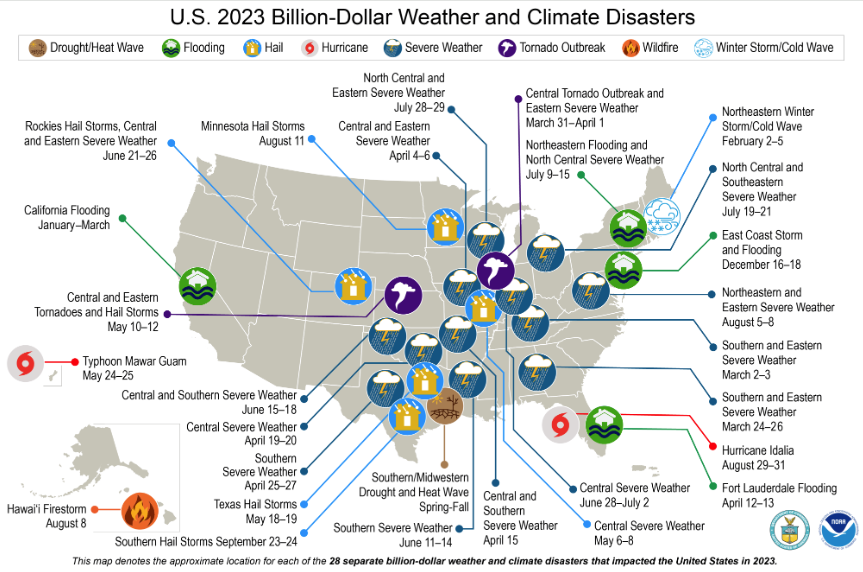

The National Centers for Environmental Information reports that the U.S. has sustained 383 weather and climate disasters since 1980, during which overall damages/costs reached or exceeded $1 billion (including CPI adjustment to 2024). The total cost of these 383 events exceeds $2.720 trillion. See graphic below.

Some might argue we are facing a crisis caused by natural disasters. However, the real crisis relates more to failings in the physical and social infrastructure designed to deal with weather-related catastrophes. This includes the insurability of physical assets such as homes and industries.

Many factors contribute to the rising number and severity of extreme weather events. Warming ocean temperatures have altered usual patterns of atmospheric moisture, which in turn have caused drought conditions that have affected agricultural yields, dried out vast areas of boreal forests, and dangerous heat waves that have endangered the health of millions of city dwellers worldwide. Higher temperatures and increased atmospheric moisture can fuel stronger, longer-lasting storms.

Mitigation and recovery efforts related to wildfires, floods, storms, heat waves, and frigid temperatures have put enormous pressure on private and public financial and human resources and have caused many insurance companies to curtail or cut insurability benefits in many areas.

These changing climate-related realities have prompted governmental and industry exports to reconsider and revise the designs and standards of physical and social infrastructure needed to minimize or eliminate the risks of catastrophic failures in times of emergency. The challenges of altering new or existing infrastructure’s designs and physical attributes are mind-blowing.

Managing surface water drainage alone could lead to enormous expenditures to expand or alter drainage systems that, in many communities, have proven incapable of dealing with excessive rainfalls associated with atmospheric rivers,

Protecting homes and other buildings adjacent to forest areas vulnerable to wildfires has prompted governments and insurance providers to publish guidelines that could help to minimize damage in times of stress. Similar adaptive measures are being promulgated for homes and businesses adjacent to ocean shorelines that are at risk of storm surges or rising sea levels,

The need to lower the risks of changing climate conditions has added a new imperative to the search for sustainability. Risk assessments and the development of countervailing measures regarding policies and standards have gained added importance regarding design standards and the choice of building materials.

Where environmental impacts once guided architectural and engineering designs, the need to promote resiliency and lower the lifespan carbon footprint of fixed infrastructure has become increasingly important for business and governmental decision-makers. Reducing the environmental costs of climate-related damage and disaster mitigation alone counts significantly in the carbon accounting metrics.

Buildings constructed with flammable materials and few fire prevention features are being reevaluated and renovated to lower the risk of exposure to excessive heat and fire hazards. Similarly, earlier design features that were less able to withstand earthquakes are being updated to forestall catastrophic collapses when tectonic events occur.

Research has shown that changes to building codes offer a rare opportunity to lower disaster liability and minimize long-term ownership costs.

The US Resiliency Council successfully led the effort to create a new $250 million grant fund to help retrofit thousands of earthquake-vulnerable apartment buildings throughout California. As many as 100,000 California soft-story apartment buildings house up to 2.5 million people, often elderly, minority, and low—to moderate-income working families.

Designing for resiliency has important implications for insurability. Faced with mounting payout costs for homes and factories damaged by floods, fires, storms, or earthquakes, many insurance providers have cut or lowered the availability of coverage for areas deemed vulnerable to climate-related catastrophes. In other cases, the prices for insurance coverage have risen sharply when design features or building materials being used have been deemed to be at risk.

For example, Insurance underwriters, property managers, and government officials recognize that insurance coverage for the construction of mass timber buildings is much higher than for most other building types.

A new era of heightened climate-related hazard risk is emerging. It will require greater collaboration between policymakers, regulators, engineers, and architects to design and build the physical infrastructure and social networks necessary to reduce communities’ and industries’ exposure to catastrophic failures. The change will not happen quickly, but it must happen because Resilience is the new face of sustainability.

_____________________________________________

Frank Came is an independent communications and policy consultant with extensive experience with national and international clients on sustainability and environmental matters and serves as the Editor of Globe-Net. You may contact Frank c/o frank.came@globe.ca